Life Insurance 2026: Essential for Your Financial Future

The Indispensable Role of Life Insurance in Your 2026 Financial Plan: A Comprehensive Guide

As we navigate the complexities of modern life, the importance of robust financial planning cannot be overstated. With 2026 on the horizon, it’s crucial to reassess and reinforce your financial strategies to ensure both your present stability and future security. At the core of any resilient financial plan lies a fundamental yet often misunderstood component: life insurance. This comprehensive guide will delve into why life insurance 2026 is not just a safety net, but a cornerstone of holistic financial well-being, offering practical solutions and insights for individuals and families alike.

Many people view life insurance as a morbid necessity, something to consider only when they are older or have significant dependents. However, this perception significantly underestimates its multifaceted benefits. Life insurance, when strategically integrated into your financial plan, serves as a powerful tool for wealth protection, estate planning, and even wealth accumulation, depending on the type of policy. Understanding its nuances and how it aligns with your long-term goals is paramount for making informed decisions in the coming years.

The economic landscape is constantly evolving, bringing with it new challenges and opportunities. From inflation to market volatility, external factors can significantly impact your financial outlook. Life insurance provides a layer of certainty in an uncertain world, guaranteeing financial support for your loved ones when they need it most. This article aims to demystify life insurance 2026, exploring its various forms, benefits, and how to choose the right policy to meet your unique needs.

Why Life Insurance is More Critical Than Ever for Your 2026 Financial Plan

The year 2026 brings with it a renewed focus on individual and family financial resilience. Economic shifts, healthcare costs, and the general unpredictability of life underscore the growing importance of proactive financial measures. Life insurance addresses several critical aspects of financial planning that are often overlooked:

- Income Replacement: In the event of your untimely passing, life insurance provides a financial cushion for your dependents, replacing lost income and ensuring they can maintain their standard of living. This is especially critical for primary wage earners.

- Debt Protection: Outstanding debts, such as mortgages, car loans, and credit card balances, can become a significant burden for your family. A life insurance payout can cover these liabilities, preventing foreclosure or financial distress.

- Education Funding: For families with children, life insurance can guarantee funds for future educational expenses, from college tuition to vocational training, regardless of unforeseen circumstances.

- Estate Planning & Inheritance: It can be a vital tool for estate equalization, ensuring all heirs receive a fair share, or for leaving a tax-free inheritance to your beneficiaries.

- Business Continuity: For business owners, life insurance can fund buy-sell agreements, protect against the loss of a key employee, or provide liquidity for business transitions.

- Charitable Giving: Many individuals use life insurance to leave a substantial legacy to their favorite charities, making a significant impact beyond their lifetime.

Considering these points, it becomes clear that life insurance 2026 is not just about protecting against the worst-case scenario, but about empowering your family to pursue their dreams and maintain their financial footing even in your absence. It’s an act of love and responsibility that provides unparalleled peace of mind.

Understanding the Landscape: Types of Life Insurance for 2026

Navigating the various types of life insurance can be daunting, but understanding the core differences is key to selecting the right policy. For your life insurance 2026 strategy, consider these main categories:

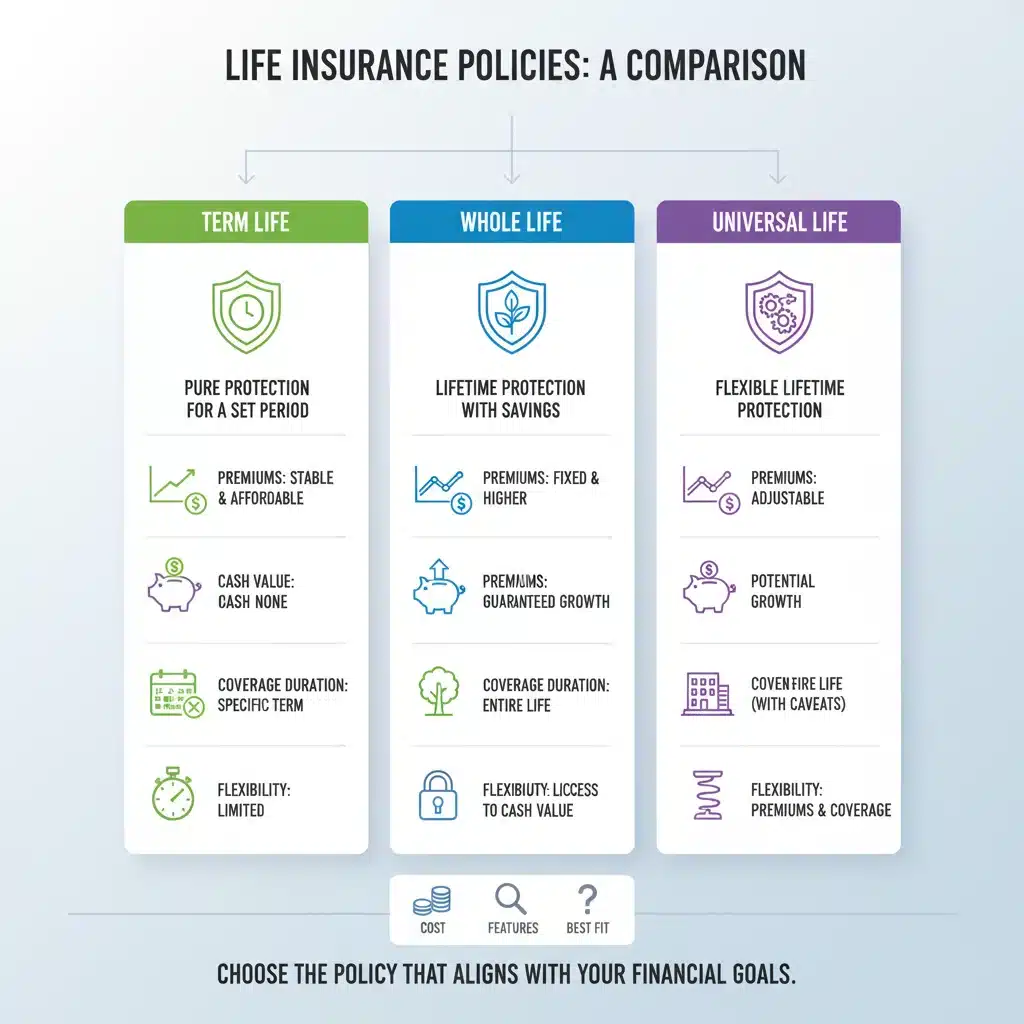

1. Term Life Insurance

Term life insurance is often considered the simplest and most affordable option. It provides coverage for a specific period, or ‘term,’ typically 10, 20, or 30 years. If the insured person passes away within the policy term, a death benefit is paid to the beneficiaries. If they outlive the term, the policy expires, and no payout is made. This type of insurance is ideal for:

- Individuals seeking coverage for a specific duration, such as when they have young children or a mortgage.

- Those who want maximum coverage at the lowest initial cost.

- People who anticipate their financial obligations will decrease over time.

Renewable term policies allow you to extend coverage at the end of the term, though premiums will likely increase due to age. Convertible term policies offer the option to convert to a permanent policy later, without requiring a new medical exam.

2. Whole Life Insurance

Whole life insurance is a type of permanent life insurance that provides coverage for the entire lifetime of the insured, as long as premiums are paid. It features a guaranteed death benefit, guaranteed premiums, and a cash value component that grows over time on a tax-deferred basis. This cash value can be accessed through withdrawals or loans, offering a source of liquidity during your lifetime. Whole life is suitable for:

- Individuals looking for lifelong coverage and guaranteed benefits.

- Those who want a savings component within their policy.

- People interested in estate planning or leaving a guaranteed inheritance.

While premiums are generally higher than term life, the guarantees and cash value accumulation make it an attractive option for long-term financial security.

3. Universal Life Insurance

Universal life (UL) insurance is another form of permanent life insurance, offering more flexibility than whole life. Policyholders can adjust their premiums and death benefits within certain limits. It also has a cash value component that grows based on an interest rate set by the insurer, which can fluctuate. There are several variations of universal life, including:

- Guaranteed Universal Life (GUL): Offers lifelong coverage with guaranteed premiums and death benefits, similar to whole life, but often with less emphasis on cash value growth.

- Indexed Universal Life (IUL): The cash value growth is tied to the performance of a stock market index, offering potential for higher returns, but also with caps and floors to limit risk.

- Variable Universal Life (VUL): Allows policyholders to invest the cash value in sub-accounts, similar to mutual funds. This offers the highest potential for growth but also carries the most risk, as the cash value can decrease if investments perform poorly.

Universal life policies are ideal for those who desire lifelong coverage with greater flexibility in premium payments and death benefits, and who may be comfortable with some level of investment risk depending on the specific UL variant.

Key Considerations When Choosing Your Life Insurance 2026 Policy

Selecting the right life insurance 2026 policy involves more than just picking a type. Several factors should influence your decision to ensure the coverage aligns perfectly with your financial goals and personal circumstances:

1. Your Current Life Stage and Future Goals

Your needs will vary significantly depending on your life stage. A young professional with no dependents might opt for a smaller term policy to cover potential future debts, while a couple with young children and a mortgage will likely need substantial term coverage. As you approach retirement, permanent life insurance might become more appealing for estate planning purposes or to supplement retirement income through cash value access.

2. Financial Dependents and Their Needs

The primary purpose of life insurance is to protect your financial dependents. Consider:

- How many people rely on your income?

- What are their current and future financial needs (e.g., daily living expenses, education, healthcare)?

- How long would they need financial support in your absence?

A common guideline is to aim for coverage that is 7-10 times your annual income, but a more detailed assessment based on specific expenses and future obligations is always recommended.

3. Existing Debts and Liabilities

Factor in all your outstanding debts. This includes your mortgage, car loans, student loans, and any other significant liabilities. Your life insurance policy should ideally cover these to prevent your family from inheriting a financial burden.

4. Budget and Affordability

While adequate coverage is important, it must also be affordable. Don’t overextend yourself on premiums, as lapsing a policy due to non-payment is detrimental. Balance your desired coverage with what you can comfortably pay each month or year. Remember, even a modest policy is better than no policy at all.

5. Health and Lifestyle

Your health status, age, and lifestyle choices (e.g., smoking, dangerous hobbies) significantly impact premiums. It’s generally advisable to purchase life insurance when you are younger and healthier, as this locks in lower rates. Be honest about your health history during the application process to avoid claim denials later on.

6. Riders and Additional Benefits

Many policies offer riders that can customize your coverage. Common riders include:

- Waiver of Premium Rider: Waives premiums if you become totally disabled.

- Accelerated Death Benefit Rider: Allows you to access a portion of the death benefit while still alive if you are diagnosed with a terminal illness.

- Child Rider: Provides a small amount of coverage for your children.

- Guaranteed Insurability Rider: Allows you to purchase additional coverage in the future without a medical exam.

Evaluate which riders might be beneficial for your specific situation.

Integrating Life Insurance into Your 2026 Financial Plan: Practical Strategies

Once you understand the types and considerations, the next step is to seamlessly integrate life insurance 2026 into your broader financial strategy. Here’s how:

1. Conduct a Needs Analysis

This is the foundational step. Work with a financial advisor or use online calculators to determine exactly how much coverage you need. Consider your income, debts, future expenses (e.g., college), and any existing assets or savings that could offset needs. Don’t forget final expenses like funeral costs.

2. Review Annually or After Major Life Events

Your life insurance needs are not static. Major life events such as marriage, the birth of a child, purchasing a home, starting a business, or a significant increase/decrease in income should prompt a review of your policy. What was sufficient in 2023 might not be enough for 2026. An annual review ensures your coverage remains appropriate.

3. Understand the Tax Implications

Generally, life insurance death benefits are paid out income tax-free to beneficiaries. However, there can be estate tax implications for very large policies. Cash value growth in permanent policies is typically tax-deferred. Consult with a tax professional to understand how life insurance fits into your overall tax strategy.

4. Coordinate with Other Financial Instruments

Life insurance should not exist in a vacuum. It should complement your other financial tools, such as retirement accounts (401k, IRA), investment portfolios, and savings. For instance, term life can provide protection during peak earning years, allowing you to aggressively save for retirement. Permanent life insurance can offer a tax-efficient way to diversify your assets.

5. Consider Laddering Term Policies

If you have varying financial obligations over time, consider a ‘term ladder’ strategy. This involves purchasing multiple term policies of different durations and amounts. For example, a 30-year policy for your mortgage, a 20-year policy for your children’s education, and a 10-year policy for short-term income replacement. This can be more cost-effective than a single large, long-term policy.

6. Don’t Delay

The younger and healthier you are, the lower your premiums will be. Delaying the purchase of life insurance means you’ll pay more later, and there’s always the risk of developing a health condition that could make coverage more expensive or even unobtainable. Act proactively to secure your life insurance 2026 needs.

Common Myths and Misconceptions About Life Insurance

Despite its importance, life insurance is often surrounded by myths that deter people from obtaining adequate coverage. Let’s debunk some common misconceptions as we look towards life insurance 2026:

Myth 1: I’m Young and Healthy, I Don’t Need It Yet.

Reality: This is precisely the best time to get life insurance! Premiums are significantly lower when you’re young and healthy, and you lock in those rates for the duration of your policy (especially with permanent options). An unexpected illness or accident can happen at any age, leaving dependents vulnerable.

Myth 2: It’s Too Expensive.

Reality: Many people overestimate the cost of life insurance, particularly term life. A healthy 30-year-old might be surprised at how affordable a substantial term policy can be. While permanent policies are more expensive, they offer lifelong coverage and cash value growth, making them a valuable asset.

Myth 3: I Have Life Insurance Through My Employer, So I’m Covered.

Reality: Group life insurance through an employer is a great benefit, but it’s often insufficient. Coverage amounts are typically 1-2 times your annual salary, which may not be enough to cover all your family’s financial needs. Furthermore, employer-provided policies are usually not portable, meaning you lose coverage if you leave your job. Personal life insurance 2026 provides stable, portable coverage tailored to your specific needs.

Myth 4: Only Breadwinners Need Life Insurance.

Reality: Stay-at-home parents or non-working spouses provide invaluable services (childcare, household management) that would be costly to replace. If they were to pass away, the surviving spouse would likely face significant expenses for these services. Life insurance for non-working spouses is a crucial part of comprehensive family protection.

Myth 5: Life Insurance is Only for Rich People.

Reality: Life insurance is arguably more critical for middle and lower-income families who have fewer assets to fall back on in an emergency. It provides a safety net that ensures their loved ones won’t face financial hardship when the unexpected occurs.

Dispelling these myths is crucial for making informed decisions about your financial future and ensuring your life insurance 2026 plan is robust and effective.

The Future of Life Insurance: Trends for 2026 and Beyond

The life insurance industry is not static; it’s continuously evolving, driven by technological advancements, changing consumer expectations, and new data analytics. Here’s what to expect in the realm of life insurance 2026 and beyond:

1. Personalized Underwriting

Expect more personalized underwriting processes. Insurers are increasingly using data from wearables, health apps, and electronic health records (with consent) to offer more tailored premiums based on individual health and lifestyle, potentially leading to faster approvals and more accurate pricing.

2. Digitization and AI

The application and claims processes will become even more streamlined through digitization and artificial intelligence. AI-powered chatbots for customer service, online application portals, and digital policy management will enhance the customer experience and efficiency.

3. Hybrid Products

The market will see a rise in hybrid products that combine life insurance with other benefits, such as long-term care or critical illness coverage. These integrated policies offer comprehensive protection under a single premium, addressing multiple risks simultaneously.

4. Focus on Wellness Programs

Many insurers are already incorporating wellness programs that reward policyholders for healthy behaviors with lower premiums or other incentives. This trend is expected to grow, shifting the focus from just protection to prevention and overall well-being.

5. Greater Transparency and Simplicity

As consumers demand more clarity, insurers will likely offer more transparent policy terms and simpler products, making it easier for individuals to understand what they are buying and how it benefits them.

These trends indicate a future where life insurance is more accessible, personalized, and integrated into a proactive approach to health and financial management. Staying informed about these developments will help you optimize your life insurance 2026 strategy.

Conclusion: Securing Your Legacy with Life Insurance in 2026

As you plan for 2026 and the years that follow, remember that life insurance is far more than just a financial product; it’s a profound commitment to the well-being of those you love. It offers a promise of financial stability, debt relief, and the pursuit of future dreams, even in your absence. By understanding the different types of policies, carefully assessing your needs, and integrating life insurance strategically into your overall financial plan, you can build a robust foundation for your family’s future.

Don’t fall prey to common myths or procrastinate on this vital decision. The sooner you address your life insurance 2026 needs, the more affordable and comprehensive your coverage will be. Consult with a qualified financial advisor to tailor a plan that aligns with your unique circumstances, budget, and long-term aspirations. Investing in life insurance today is investing in peace of mind, ensuring that your legacy is one of security, care, and unwavering support for your loved ones, no matter what tomorrow brings.

Take the proactive step today to secure your family’s financial future. Life insurance isn’t just about what happens when you’re gone; it’s about the continued life and opportunities of those you leave behind. Make life insurance 2026 a priority in your financial planning.