Maximizing 2026 Charitable Giving: Tax-Efficient Donations

Strategic financial planning in 2026 allows individuals to significantly amplify their philanthropic impact by leveraging advanced tax-efficient donation techniques, optimizing both charitable contributions and personal financial outcomes.

As we navigate the evolving financial landscape of 2026, understanding how to maximize your charitable contributions while simultaneously optimizing your tax position is more crucial than ever. This guide delves into advanced financial planning techniques designed to make your donations truly impactful and tax-efficient, ensuring your generosity goes further.

Strategic Overview of 2026 Charitable Giving Landscape

The year 2026 brings with it specific tax considerations and opportunities that can significantly influence how individuals approach philanthropic endeavors. A strategic overview of this landscape is essential for anyone looking to make a meaningful difference while also benefiting from available tax incentives. Understanding these nuances allows for a more deliberate and impactful approach to giving.

Current tax laws, including potential adjustments to standard deductions and itemized deduction limitations, play a pivotal role. High-net-worth individuals, in particular, stand to gain substantially from sophisticated planning that aligns their charitable intent with their financial objectives. This involves not just giving cash, but considering a broader array of assets and giving vehicles.

Understanding the Tax Implications

Before diving into specific strategies, it’s vital to grasp the fundamental tax implications of charitable giving in 2026. This includes:

- Adjusted Gross Income (AGI) Limits: Knowing the percentage of your AGI that can be deducted for cash versus non-cash contributions.

- Itemized Deductions: Whether itemizing deductions or taking the standard deduction provides a greater tax advantage.

- State-Specific Incentives: Exploring any state-level tax credits or deductions for charitable contributions that might complement federal benefits.

By carefully evaluating these parameters, donors can tailor their giving strategy to achieve maximum tax efficiency. This foundational understanding is the first step towards truly maximizing your philanthropic impact in the current financial climate.

Ultimately, a comprehensive strategic overview ensures that every charitable dollar is optimized for both the recipient organization and the donor’s financial health. It’s about making informed choices that resonate with your values and financial goals.

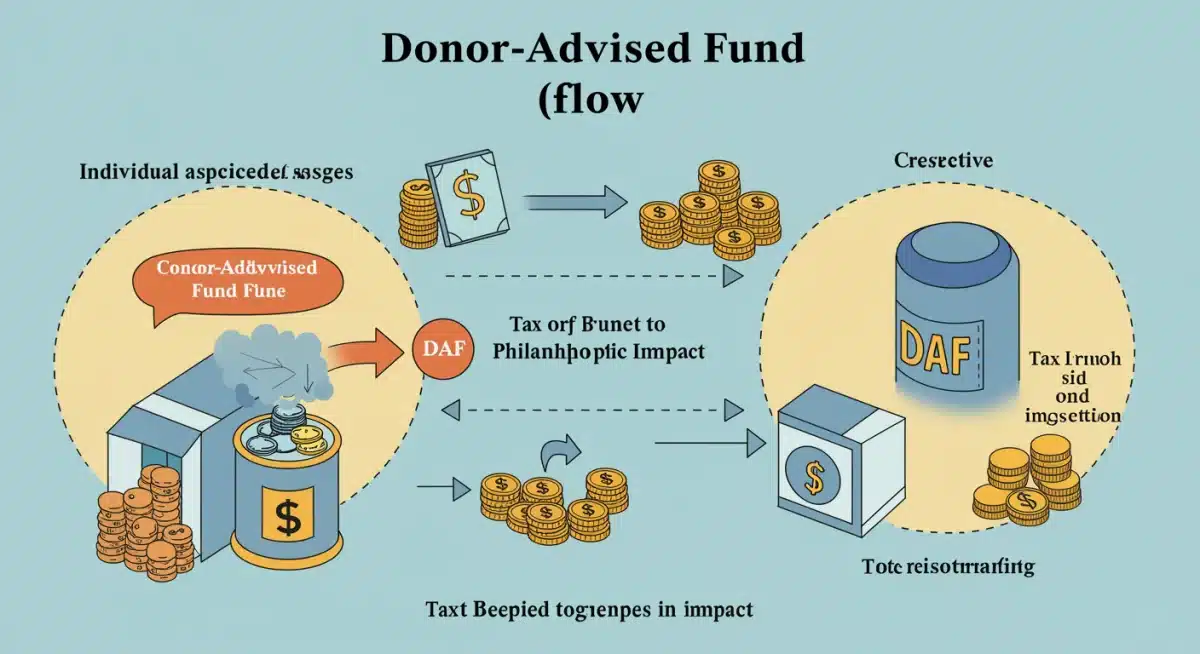

Leveraging Donor-Advised Funds (DAFs) for Enhanced Giving

Donor-Advised Funds (DAFs) have emerged as a powerful tool for philanthropic individuals seeking flexibility, tax advantages, and a streamlined approach to giving. In 2026, DAFs continue to offer compelling benefits, particularly for those looking to make substantial contributions without immediately designating specific charities.

A DAF allows you to make an irrevocable charitable contribution to a sponsoring organization, receive an immediate tax deduction, and then recommend grants from the fund to qualified charities over time. This separation of the donation date from the grant-making date provides significant strategic advantages, especially for managing income spikes or planning for future giving.

Key Benefits of DAFs in 2026

The appeal of DAFs extends beyond simple tax deductions. They offer a sophisticated framework for sustained philanthropy. Consider these benefits:

- Immediate Tax Deduction: You receive a tax deduction in the year you contribute to the DAF, regardless of when the grants are made to charities.

- Simplified Record-Keeping: The sponsoring organization handles all administrative tasks and record-keeping for your donations.

- Anonymity: If desired, you can recommend grants to charities anonymously, protecting your privacy.

- Investment Growth: Funds in a DAF can be invested and grow tax-free, allowing for potentially larger grants over time.

DAFs are particularly advantageous when donating appreciated assets, as they allow you to avoid capital gains taxes while receiving a fair market value deduction. This makes them an excellent vehicle for individuals with significant holdings in stocks, mutual funds, or even certain private assets.

The strategic use of DAFs in 2026 can transform reactive giving into proactive philanthropy, enabling donors to plan their impact more effectively and manage their tax obligations with greater foresight. It’s a versatile tool for both episodic large donations and ongoing charitable commitments.

Optimizing with Qualified Charitable Distributions (QCDs)

For individuals aged 70½ or older, Qualified Charitable Distributions (QCDs) represent a highly effective strategy for tax-efficient giving from Individual Retirement Accounts (IRAs). In 2026, QCDs remain a powerful tool for satisfying Required Minimum Distributions (RMDs) while supporting beloved charitable causes, potentially reducing taxable income.

A QCD allows you to directly transfer funds from your IRA to an eligible charity. This direct transfer is excluded from your gross income, which can be particularly beneficial for those who do not itemize deductions. It effectively lowers your adjusted gross income, which can have ripple effects on other tax considerations, such as Medicare premiums.

Maximizing QCD Impact

To fully leverage QCDs, understanding their specific rules and limitations is key. Here are important aspects to consider:

- Age Requirement: You must be 70½ or older to make a QCD.

- Direct Transfer: Funds must go directly from your IRA custodian to the charity. Money withdrawn by you and then donated does not qualify.

- Eligible Charities: Most 501(c)(3) public charities are eligible, but DAFs and private foundations are generally not.

- Annual Limit: There is an annual limit on QCDs, which is subject to inflation adjustments each year. Staying informed about the 2026 limit is crucial.

QCDs are particularly attractive because they reduce your taxable income dollar-for-dollar, unlike a charitable deduction which only reduces your taxable income if you itemize. This makes them a universally beneficial strategy for eligible seniors, regardless of their itemizing status.

By incorporating QCDs into your 2026 financial plan, you can strategically fulfill your RMD obligations, support charities close to your heart, and potentially reduce your overall tax burden, making it a win-win scenario for both donor and recipient.

Strategic Giving of Appreciated Assets

Donating appreciated assets, such as stocks, mutual funds, or real estate, is one of the most powerful and often underutilized strategies for maximizing charitable giving in a tax-efficient manner. In 2026, this approach continues to offer significant advantages over simply donating cash, especially for individuals with long-term capital gains.

When you donate appreciated assets held for more than one year, you typically avoid paying capital gains tax on the appreciation. Furthermore, you can usually deduct the fair market value of the asset on the date of the donation. This dual benefit—avoiding capital gains and receiving a substantial deduction—makes it an incredibly efficient way to give.

Types of Appreciated Assets to Consider

The range of appreciated assets suitable for charitable donations is broader than many realize. Exploring these options can unlock new levels of tax efficiency:

- Publicly Traded Securities: Stocks, bonds, and mutual funds that have increased significantly in value since purchase.

- Real Estate: Homes, land, or commercial properties that have appreciated, though this often involves more complex transactions.

- Privately Held Stock: Shares in a privately held company, which can offer significant tax advantages but require careful valuation.

- Collectibles: Art, antiques, or other valuable items, though their deduction value may be limited to their cost basis if the charity’s use is unrelated to its exempt purpose.

The key is to identify assets with significant unrealized gains that you no longer wish to hold. By donating these directly to charity, you bypass the capital gains tax you would incur if you sold them and then donated the cash proceeds. This can result in a much larger donation to the charity and a greater tax benefit for you.

Proper planning with appreciated assets requires careful consideration of the asset’s holding period, its fair market value, and the specific rules governing non-cash contributions. Consulting with a financial advisor is highly recommended to navigate these complexities and ensure optimal outcomes in 2026.

Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs)

For donors with substantial wealth and complex financial planning needs, Charitable Remainder Trusts (CRTs) and Charitable Lead Trusts (CLTs) offer sophisticated avenues for integrating philanthropy with estate planning and income generation. These advanced techniques are particularly relevant in 2026 for those seeking to leave a lasting legacy while managing current financial objectives.

A Charitable Remainder Trust (CRT) allows you to transfer assets into an irrevocable trust, receive an income stream for a specified term or for life, and then designate a charity to receive the remaining assets upon the trust’s termination. This strategy provides an immediate income tax deduction for the present value of the charitable remainder interest, avoids capital gains taxes on appreciated assets transferred to the trust, and removes the assets from your taxable estate.

Contrasting CRTs and CLTs

While both CRTs and CLTs involve charitable giving through trusts, their mechanisms and primary benefits differ significantly:

- Charitable Remainder Trust (CRT):

- Donor receives income first, charity receives remainder.

- Provides an immediate income tax deduction.

- Ideal for those needing income from appreciated assets.

- Charitable Lead Trust (CLT):

- Charity receives income first, donor (or heirs) receives remainder.

- Offers estate and gift tax benefits, and sometimes an income tax deduction.

- Suitable for those wanting to reduce taxable estate while supporting charity.

A Charitable Lead Trust (CLT), conversely, pays an income stream to a charity for a specified term, after which the remaining assets revert to the donor or their non-charitable beneficiaries. CLTs are often used as an estate planning tool, allowing donors to reduce the taxable value of assets passed to heirs while providing significant support to charities during the trust’s term.

Deciding between a CRT and a CLT depends on your specific financial situation, income needs, and estate planning goals. Both require careful legal and financial guidance to establish and manage effectively, ensuring they align with your philanthropic vision and tax objectives for 2026 and beyond.

Strategic Bunching and Qualified Appraisal Rules

Effective charitable giving in 2026 extends beyond selecting the right vehicle; it also involves strategic timing and adherence to specific IRS regulations, particularly concerning bunching deductions and qualified appraisal rules for non-cash contributions. These tactics can significantly amplify your tax benefits.

Bunching deductions involves consolidating several years’ worth of charitable contributions into a single tax year. This strategy is especially valuable for individuals whose total itemized deductions hover near the standard deduction amount. By bunching, you can exceed the standard deduction in one year, benefiting from itemizing, and then take the standard deduction in subsequent years, effectively maximizing your deductions over time.

Navigating Appraisal Requirements

When donating non-cash assets, particularly those with significant value, understanding and adhering to qualified appraisal rules is paramount to securing your tax deduction. These rules are stringent and designed to prevent overvaluation:

- Appraisal Requirement: For non-cash contributions exceeding a certain value (e.g., typically over $5,000 for most property, higher for publicly traded securities), a qualified appraisal is generally required.

- Qualified Appraiser: The appraisal must be conducted by a qualified appraiser who is independent of both the donor and the charity.

- Timely Appraisal: The appraisal must be obtained no earlier than 60 days before the donation date and no later than the due date of the tax return on which the deduction is claimed.

- IRS Form 8283: Non-cash contributions requiring an appraisal must be reported on IRS Form 8283, and the appraiser’s signature is often required.

The bunching strategy works particularly well when combined with a Donor-Advised Fund (DAF). You can make a large contribution to your DAF in a bunching year, claim the deduction, and then distribute grants to charities from your DAF over several years, maintaining consistent support for your chosen causes.

Adhering to qualified appraisal rules ensures the validity of your deduction when donating valuable non-cash assets. Failure to comply can result in the disallowance of your deduction. Therefore, meticulous record-keeping and professional guidance are indispensable components of strategic charitable giving in 2026.

Integrating Charitable Giving with Estate Planning

For many, charitable giving is not merely an annual tax strategy but a fundamental component of their legacy and estate plan. In 2026, integrating philanthropic goals with estate planning ensures that your values continue to impact the world long after you’re gone, often with significant tax advantages for your heirs.

This integration involves thoughtful consideration of how assets will be distributed upon your passing, minimizing estate taxes, and maximizing the benefit to your chosen charities. It’s about creating a comprehensive plan that reflects your deepest convictions and financial wisdom.

Key Estate Planning Tools for Philanthropy

Several estate planning vehicles can be strategically employed to facilitate charitable giving, offering both flexibility and tax efficiency:

- Bequests in Wills or Trusts: Designating a specific amount or percentage of your estate to a charity in your will or living trust. These gifts are eligible for an estate tax deduction.

- Beneficiary Designations: Naming a charity as a beneficiary of your retirement accounts (IRAs, 401(k)s) or life insurance policies. This can be highly tax-efficient, as retirement assets left to individuals are often subject to income taxes.

- Charitable Gift Annuities: A contract where you donate assets to a charity in exchange for fixed income payments for life. The remainder goes to the charity upon your death.

- Endowments and Foundations: For those with significant wealth, establishing a private foundation or contributing to an existing endowment allows for perpetual support of causes.

By carefully structuring your estate plan to include charitable components, you can reduce the size of your taxable estate, potentially lowering estate taxes owed by your heirs. This allows more of your wealth to pass to your loved ones and your chosen causes, rather than to taxes.

The process of integrating charitable giving with estate planning is complex and highly individualized. It typically involves collaboration with estate attorneys, financial advisors, and tax professionals to ensure all legal and financial aspects are meticulously addressed, aligning your philanthropic legacy with your overall financial objectives for 2026.

| Key Strategy | Brief Description |

|---|---|

| Donor-Advised Funds (DAFs) | Contribute assets for an immediate tax deduction, then recommend grants to charities over time, with investment growth. |

| Qualified Charitable Distributions (QCDs) | Individuals 70½+ can transfer IRA funds directly to charity, satisfying RMDs and reducing taxable income. |

| Appreciated Assets | Donate stocks or property held over one year to avoid capital gains tax and receive a fair market value deduction. |

| Charitable Trusts | CRTs provide income to you then charity; CLTs provide income to charity then heirs, optimizing estate taxes. |

Frequently Asked Questions About 2026 Charitable Giving

In 2026, primary tax benefits include income tax deductions for cash and non-cash contributions, avoidance of capital gains tax on appreciated asset donations, and potential estate tax reductions. Eligibility often depends on whether you itemize deductions and your Adjusted Gross Income (AGI).

A DAF allows you to contribute assets, receive an immediate tax deduction in the year of contribution, and then recommend grants to charities over time. This strategy separates the deduction from the actual grant-making, and allows invested funds to grow tax-free, maximizing future donations.

Individuals aged 70½ or older with an IRA can benefit from QCDs. They allow direct transfers from an IRA to a charity, satisfying Required Minimum Distributions (RMDs) and reducing taxable income, which is particularly advantageous for those who do not itemize deductions.

Donating appreciated securities held for over a year offers two main advantages: you avoid paying capital gains tax on the asset’s appreciation, and you can deduct the fair market value of the security. This dual benefit significantly enhances the value of your donation and your tax savings.

Charitable giving can be integrated through bequests in wills, naming charities as beneficiaries of retirement accounts or life insurance, and establishing charitable trusts. These methods can reduce estate taxes, ensure your legacy, and provide significant support to your chosen causes after your passing.

Conclusion

Maximizing your 2026 charitable giving: advanced financial planning techniques for tax-efficient donations is not merely about altruism; it’s about intelligent stewardship of your resources. By strategically employing tools like Donor-Advised Funds, Qualified Charitable Distributions, and the donation of appreciated assets, alongside thoughtful estate planning, you can significantly amplify your philanthropic impact while optimizing your personal tax situation. The evolving financial landscape of 2026 presents unique opportunities for informed donors to make a profound difference, ensuring their generosity is both powerful and financially sound. Consulting with financial and tax professionals remains paramount to tailoring these strategies to your specific circumstances and achieving your charitable and financial goals.

and IRA in 2025")