2026 Estate Planning Guide: Navigating New Regulations for Asset Protection

Estate planning is not merely a task for the wealthy; it is a crucial component of financial wellness for everyone. As we look towards 2026, the landscape of estate planning continues to evolve, bringing with it new regulations, opportunities, and challenges. Navigating these changes effectively is paramount to ensuring your assets are protected, your wishes are honored, and your legacy is securely passed on to future generations. This comprehensive guide delves into the intricacies of 2026 Estate Planning, offering practical solutions and insights to help you make informed decisions.

The year 2026 is significant due to potential shifts in tax laws, particularly concerning estate and gift taxes. The sunsetting provisions of the Tax Cuts and Jobs Act (TCJA) of 2017 are set to expire, potentially reverting the estate tax exemption amounts to pre-2018 levels, adjusted for inflation. This impending change necessitates a proactive approach to estate planning, especially for individuals and families with substantial assets. Understanding these potential shifts and their implications is the first step in crafting a resilient estate plan.

The Shifting Sands of Estate Tax Exemptions in 2026 Estate Planning

One of the most talked-about aspects of 2026 Estate Planning revolves around the federal estate tax exemption. Currently, the exemption is historically high, allowing individuals to transfer a significant amount of wealth free from federal estate tax. However, without legislative action, this exemption is scheduled to be cut roughly in half in 2026. This reduction could bring many more estates into the federal estate tax net, making strategic planning more critical than ever.

For high-net-worth individuals, this potential change presents both a challenge and an opportunity. The challenge lies in minimizing potential estate tax liability under a lower exemption. The opportunity, however, is to utilize the current higher exemption amounts while they are still available. Gifting strategies, such as making substantial gifts to beneficiaries now, can effectively remove assets from your taxable estate before the exemption decreases. This ‘use it or lose it’ mentality is driving many to re-evaluate their current estate plans.

It’s important to remember that state estate and inheritance taxes also play a significant role. While federal laws often take center stage, many states impose their own taxes, sometimes with much lower exemption thresholds than the federal government. A thorough 2026 Estate Planning strategy must consider both federal and state regulations to provide truly comprehensive asset protection. Consulting with an estate planning attorney familiar with both federal and state laws is crucial to understanding your specific exposure and options.

Understanding the Mechanics of Estate Tax

To effectively plan for 2026, it’s vital to grasp how estate tax works. The federal estate tax is a tax on your right to transfer property at your death. It consists of an accounting of everything you own or have certain interests in at the date of death. The fair market value of these items is used, not necessarily what you paid for them or what their values were when you acquired them. The total of these items is your ‘gross estate’.

Certain deductions are allowed from the gross estate, such as mortgages and other debts, administration expenses, property that passes to surviving spouses, and charitable donations. After these deductions are taken, the resulting amount is your ‘taxable estate’. The unified credit (which is tied to the exemption amount) is then applied to reduce or eliminate the estate tax liability. As the exemption amount changes, so does the effectiveness of this credit.

Gift tax is closely linked to estate tax. The federal gift tax is a tax on the transfer of property by one individual to another while receiving nothing, or less than full value, in return. The gift tax and estate tax share a unified credit. This means that if you use part of your lifetime exemption to make large gifts during your lifetime, it reduces the amount of exemption available at your death. Understanding this interplay is fundamental for effective 2026 Estate Planning.

Core Components of a Robust 2026 Estate Plan

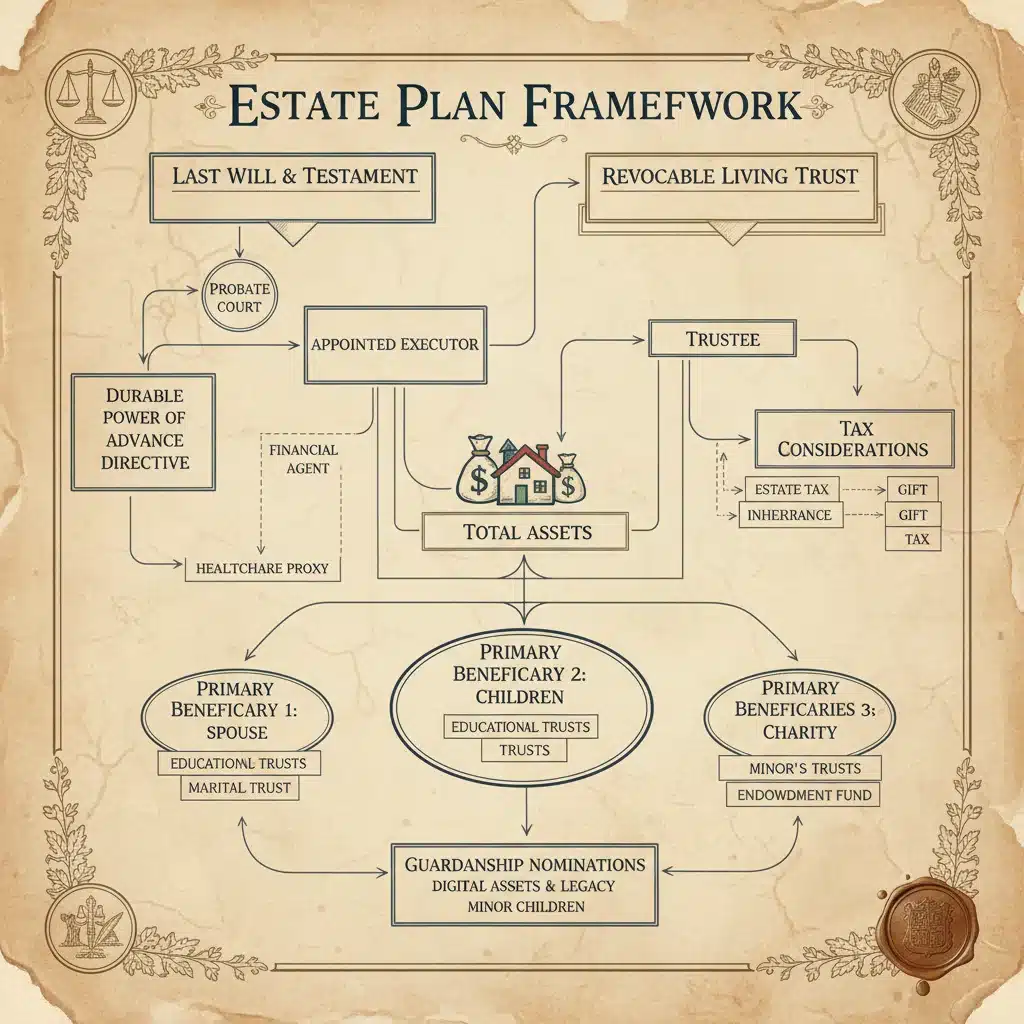

Regardless of tax law changes, the foundational elements of a sound estate plan remain critical. For 2026 Estate Planning, these components need to be reviewed and potentially updated to align with current laws and your evolving personal circumstances. A comprehensive plan typically includes a will, trusts, powers of attorney, and healthcare directives.

The Indispensable Will

A will is the cornerstone of any estate plan. It dictates how your assets will be distributed after your death, names guardians for minor children, and appoints an executor to manage your estate. Without a valid will, your assets will be distributed according to state intestacy laws, which may not align with your wishes. For 2026 Estate Planning, ensure your will is up-to-date, reflects your current assets and beneficiaries, and addresses any specific bequests you wish to make.

The Power and Flexibility of Trusts

Trusts offer a higher degree of control and flexibility than wills, especially in the context of asset protection and tax planning. They can help avoid probate, reduce estate taxes, protect assets from creditors, and provide for beneficiaries with special needs. There are numerous types of trusts, each serving a specific purpose:

- Revocable Living Trusts: These trusts can be changed or revoked during your lifetime. They help avoid probate and provide for seamless asset management if you become incapacitated.

- Irrevocable Trusts: Once established, these trusts generally cannot be modified or revoked without the consent of the beneficiary. They are powerful tools for estate tax planning, asset protection, and charitable giving, as assets placed in an irrevocable trust are typically removed from your taxable estate. Given the potential changes in 2026, irrevocable trusts may become even more attractive for wealth transfer.

- Special Needs Trusts: Designed to provide for individuals with disabilities without jeopardizing their eligibility for government benefits.

- Charitable Trusts: Allow you to support causes you care about while potentially reducing estate and income taxes.

Choosing the right trust or combination of trusts requires careful consideration of your financial situation, family dynamics, and estate planning goals. For high-net-worth individuals, exploring irrevocable trust options in 2024 and 2025 could be a strategic move to lock in the higher exemption amounts before 2026.

Powers of Attorney and Healthcare Directives

These documents are crucial for ensuring your financial and medical affairs are managed according to your wishes if you become incapacitated. A Durable Power of Attorney grants someone the authority to make financial decisions on your behalf, while a Healthcare Power of Attorney (or Medical Proxy) designates someone to make medical decisions. An Advance Directive (or Living Will) expresses your wishes regarding medical treatment. These documents are vital for a comprehensive 2026 Estate Planning strategy, providing peace of mind and preventing potential family disputes during difficult times.

Strategic Gifting in the Face of 2026 Changes

As the potential reduction in the federal estate tax exemption looms in 2026, strategic gifting has emerged as a key tactic for many individuals. Utilizing the current higher gift tax exemption can allow you to transfer significant wealth out of your estate, effectively ‘freezing’ its value for estate tax purposes and removing future appreciation from your taxable estate.

Annual Gift Tax Exclusions

Beyond the lifetime exemption, there’s an annual gift tax exclusion, which allows you to give a certain amount to as many individuals as you wish each year, free of gift tax, and without using up any of your lifetime exemption. This amount is adjusted for inflation annually. While these individual gifts are smaller, consistently making them over several years can significantly reduce the size of your taxable estate. This is a simple yet powerful tool in 2026 Estate Planning.

Larger Lifetime Gifting Strategies

For those with substantial assets, making larger gifts that utilize part of your lifetime exemption may be advisable before 2026. This could involve direct gifts of cash, securities, or real estate. Another strategy is to fund irrevocable trusts with these gifts. Types of irrevocable trusts commonly used for gifting include:

- Grantor Retained Annuity Trusts (GRATs): These allow you to transfer appreciating assets into a trust while retaining an annuity payment for a set term. At the end of the term, any remaining assets (plus appreciation) pass to your beneficiaries free of estate and gift tax.

- Spousal Lifetime Access Trusts (SLATs): A SLAT is an irrevocable trust created by one spouse for the benefit of the other spouse and their descendants. This can be an effective way to remove assets from the grantor’s estate while still providing indirect access to the funds for the family through the beneficiary spouse.

- Dynasty Trusts (Generation-Skipping Trusts): These trusts are designed to benefit multiple generations, potentially avoiding estate taxes for several generations.

The key benefit of making these larger gifts before 2026 is that the IRS has indicated it will not ‘claw back’ gifts made under the higher exemption if the exemption amount later decreases. This provides a window of opportunity to transfer wealth under the most favorable tax rules currently available. However, such strategies require careful planning and professional guidance to avoid unintended consequences and ensure compliance with complex tax laws.

Business Succession Planning in 2026

For business owners, 2026 Estate Planning extends beyond personal assets to include the future of their enterprise. A well-crafted business succession plan ensures the smooth transition of leadership and ownership, preserving the business’s value and continuity. This is particularly crucial if the business is a significant component of your overall estate.

Key Considerations for Business Owners

- Identify Successors: Determine who will take over leadership and ownership. This could be a family member, a key employee, or an external buyer.

- Valuation: Obtain a professional valuation of your business to understand its worth and to plan for potential estate tax liabilities.

- Buy-Sell Agreements: These agreements dictate how ownership shares will be handled upon an owner’s death, disability, or retirement. They help ensure a fair price and a smooth transition.

- Gifting Business Interests: Similar to personal assets, gifting shares of your business to heirs over time can reduce the size of your taxable estate. This should be done strategically, considering control and management issues.

- Life Insurance: Life insurance policies can provide liquidity to pay estate taxes or to fund a buy-sell agreement, ensuring the business can continue operating without being forced to sell assets to cover expenses.

The potential changes in estate tax exemptions in 2026 could significantly impact the tax burden on business transfers. Proactive planning using tools like valuation discounts for minority interests or lack of marketability, if still applicable, can be powerful strategies to minimize tax liabilities. Engaging with experienced business and estate planning attorneys is essential to navigate these complexities.

Charitable Giving and 2026 Estate Planning

For many, leaving a philanthropic legacy is as important as transferring wealth to family. Charitable giving can be a powerful tool in 2026 Estate Planning, offering significant tax advantages while supporting causes you care about. Strategies for charitable giving can be integrated into your estate plan to reduce estate taxes, provide income streams, and fulfill philanthropic goals.

Popular Charitable Giving Vehicles

- Outright Bequests in a Will: A simple way to leave a specific asset or percentage of your estate to a charity. These bequests are fully deductible for estate tax purposes.

- Charitable Remainder Trusts (CRTs): You transfer assets into an irrevocable trust, which then pays you (or other non-charitable beneficiaries) an income stream for a set term or for life. When the term ends, the remaining assets go to your chosen charity. This provides an immediate income tax deduction and removes the assets from your taxable estate.

- Charitable Lead Trusts (CLTs): The opposite of a CRT, where the charity receives income payments for a set term, and then the remainder goes to your non-charitable beneficiaries. This can be beneficial for transferring assets to heirs with reduced gift and estate taxes.

- Donor-Advised Funds (DAFs): A DAF allows you to make an irrevocable contribution to a public charity that sponsors the fund, receiving an immediate tax deduction. You can then recommend grants from the fund to qualified charities over time. DAFs are flexible and can be a great way to consolidate your charitable giving.

Integrating charitable giving into your 2026 Estate Planning strategy requires careful consideration of your financial goals, philanthropic desires, and the specific tax implications of each vehicle. Working with a financial advisor and estate planning attorney can help you choose the most effective strategies to maximize your impact and minimize your tax burden.

The Role of Life Insurance in 2026 Estate Planning

Life insurance is a versatile tool in estate planning, often playing a critical role in providing liquidity, equalizing inheritances, and minimizing estate taxes. For 2026 Estate Planning, its importance may be amplified, especially if estate tax exemptions decrease.

Providing Liquidity for Estate Taxes

One of the primary benefits of life insurance is its ability to provide immediate cash to your beneficiaries upon your death. This liquidity can be crucial for paying estate taxes, administrative costs, and other final expenses without forcing your heirs to sell illiquid assets, such as real estate or a family business, at an unfavorable time. By structuring the ownership of the life insurance policy correctly (e.g., through an Irrevocable Life Insurance Trust or ILIT), the death benefit can be excluded from your taxable estate, making it an even more efficient tool for covering estate tax liabilities.

Equalizing Inheritances

If you have non-liquid assets, like a family business or a cherished piece of property, that you wish to pass to one heir, life insurance can be used to provide an equivalent inheritance to other heirs. This helps maintain family harmony and ensures fairness in your distribution plan. This is a common strategy in 2026 Estate Planning, particularly for families with complex asset portfolios.

Wealth Replacement

For those who make substantial charitable gifts during their lifetime or through their estate, life insurance can be used as a ‘wealth replacement’ strategy. You can donate assets to charity, taking advantage of immediate tax deductions, and then use some of the tax savings to fund a life insurance policy that will replace the value of the donated assets for your heirs. This allows you to achieve both philanthropic and family wealth transfer goals simultaneously.

The Importance of Regular Review and Professional Guidance

Estate planning is not a one-time event; it is an ongoing process that requires periodic review and adjustment. With the significant potential changes on the horizon for 2026 Estate Planning, reviewing your existing plan is more critical than ever. Life events such as marriage, divorce, birth of children or grandchildren, changes in financial circumstances, or the acquisition of new assets all necessitate a re-evaluation of your estate plan.

When to Review Your Estate Plan

- Every 3-5 Years: A general guideline for a routine check-up.

- Significant Life Events: Marriage, divorce, birth or adoption of a child, death of a beneficiary or executor, significant changes in health.

- Major Financial Changes: A substantial increase or decrease in wealth, sale of a business, inheritance, or significant changes in asset composition.

- Changes in Tax Law: As we are anticipating for 2026, any major legislative changes warrant an immediate review.

The Value of Professional Guidance

Navigating the complexities of 2026 Estate Planning requires the expertise of a team of professionals. An estate planning attorney can draft and update legal documents, ensuring they comply with current laws and accurately reflect your wishes. A financial advisor can help you assess your assets, model different scenarios, and integrate your estate plan with your broader financial goals. A tax advisor can provide insights into the tax implications of various strategies and help minimize your tax burden. For business owners, a business valuation expert and business succession planner are also invaluable.

Attempting to manage complex estate planning without professional help can lead to costly mistakes, unintended consequences, and disputes among beneficiaries. The investment in expert advice is often far outweighed by the peace of mind and financial benefits derived from a well-executed plan.

Conclusion: Proactive Planning for Your 2026 Estate Planning

The upcoming changes in 2026 present a critical juncture for estate planning. While the specifics of future legislation remain somewhat uncertain, the prudent course of action is proactive planning. By understanding the potential shifts in estate tax exemptions, reviewing and updating your core estate documents, exploring strategic gifting opportunities, integrating business succession, and considering charitable giving, you can position your estate for maximum protection and efficiency.

Remember, your estate plan is a living document that should evolve with your life and with the law. Don’t wait until 2026 to begin this process. Start now by consulting with experienced professionals who can guide you through the intricacies of 2026 Estate Planning, helping you to protect your assets, preserve your legacy, and ensure your loved ones are taken care of according to your wishes. The peace of mind that comes from a well-crafted estate plan is invaluable, securing not just your wealth, but also your family’s future for generations to come.